The Notional Interest Deduction Cyprus

Financing investments with equity: Corporate tax on interest income reduced up to 80%, resulting in effective taxation of 3%.

The Notional Interest Deduction on Cyprus Companies has received a positive endorsement by the EU. On November 27, 2020, the Economic and Financial Affairs Council (Ecofin) of the European Union approved the NID regime, confirming it is not “harmful” as per the EU Code of Conduct Group (Business Taxation).

Understanding Notional Interest Deduction (NID)

Introduced in 2015, the NID aims to provide tax relief to Cypriot companies that use equity rather than debt to finance their investments. This incentive is available to all companies resident in Cyprus and entities conducting business in the country.

NID is an annual deduction from the taxable profits of a Cypriot company. It is calculated based on the interest rate applied to the new capital introduced, owned, and used by the company for operational investments. This deduction is limited to 80% of the company’s taxable income, potentially reducing the effective tax rate from 12,5% to as low as 3%.

Key Features of NID

- Eligibility:

> Available to Cyprus resident companies and entities doing business in Cyprus.

> Applies to companies financed by their own equity. - Calculation:

> Based on the new equity introduced, either in cash or in-kind (subject to market value).

> is calculated on the 10-year government bond yield (as of December 31 of the preceding year) of the country where the equity is invested, plus a margin (initially 3%, increased to 5% from January 1, 2020). Cyprus defines 10-year government bond yields in other countries at least on an annual basis.

You may find the yields country by country here.

> The threshold of max. 80% Notional Interest Deduction (NID) is used as the lower limit. - Tax Advantage:

Reduces the effective tax rate significantly, depending on the level of capitalization.

Example of Notional Interest Deduction Cyprus

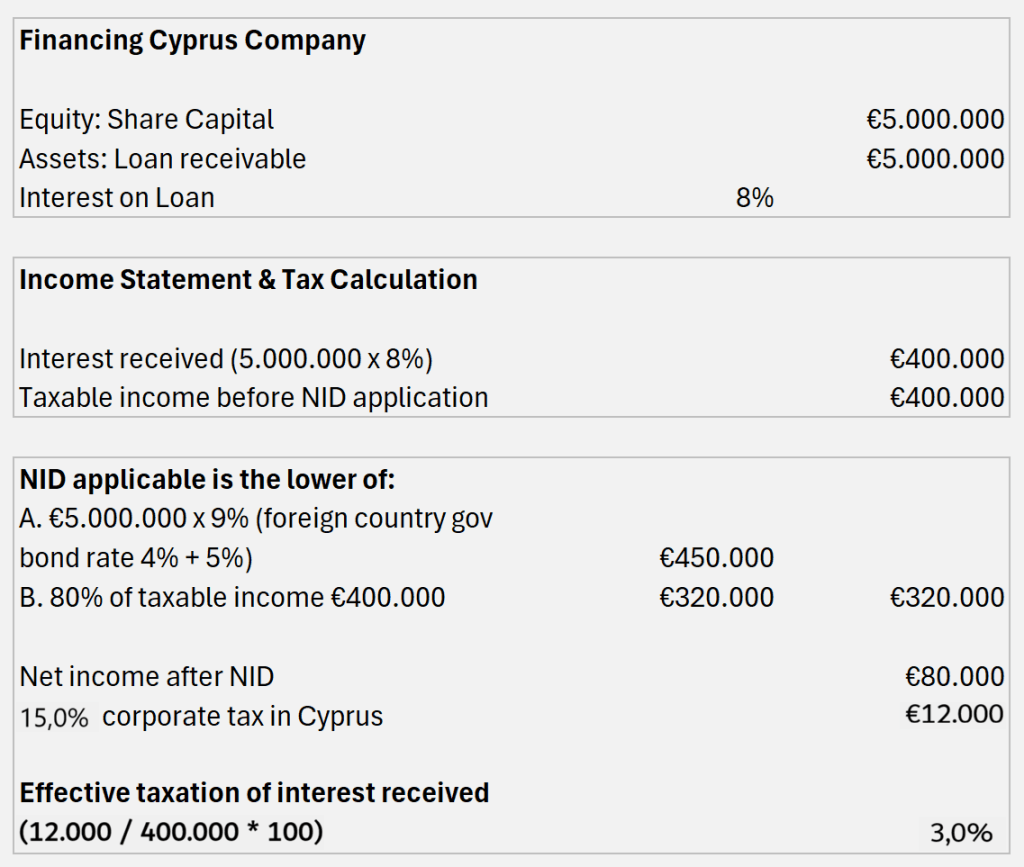

Consider a Cyprus financing company that introduces new equity of €5 million in 2023. The equity consists of fully paid share capital and share premium. The company grants an interest-bearing loan to an associated foreign company, which uses the funds to finance its operations.

NID Interest and Tax Calculation, based on the below assumptions as an example:

- The 10-year government bond yield of the foreign company’s jurisdiction is 4%.

- The Cypriot 10-year government bond yield is 2%.

- The Cyprus Company grants an interest-bearing loan to a foreign associated Company.

- The foreign associated company pays interest to the Cyprus company at a rate of 8%. (Of course, the interest rate could be 10% or 11% as well, as long as it complies with the arm-length principle.

In this scenario, the Cyprus company benefits from the NID by reducing its taxable income, thereby lowering its effective tax rate. The Cyprus company can also pay dividends to foreign investors with no Withholding Tax applying, thus further enhancing Cyprus’ appeal as an investment hub.

Tax Calculation under Notional Interest Deduction Cyprus:

Roundup

- Withholding Tax on Interest Payments to Cyprus:

Low or no withholding on interest payments in the country of the borrower, benefiting from Cyprus’ favourable double tax treaty network and EU directives. - Interest Expense Deductibility:

Interest expenses are deductible for the borrowing company, subject to its jurisdiction’s specific conditions. - Corporate Tax Rate:

If financing activities are a major business activity, the Cyprus company is subject to a corporate tax rate of 15,0% on interest income (minus NID). - Notional Interest Deduction (NID):

NID can be deducted from interest income, effectively reducing the taxable rate to 3.0% (calculated as 20% of 15,0%, with 80% given as notional interest deduction). - Dividend Payments:

Cyprus imposes no withholding tax on dividend to beneficiaries abroad payments at all.

These benefits make Cyprus an attractive jurisdiction for financing activities and international business operations.

Conclusion

The regime for Notional Interest Deduction in Cyprus offers substantial tax advantages for Cyprus companies by incentivizing equity financing. With the approval of the EU, the NID stands as a robust tool for tax planning, making Cyprus an attractive jurisdiction for business investments. For detailed advice and application of NID in specific cases, consulting with a tax professional is recommended.

For more information or assistance regarding the Notional Interest Deduction (NID) in Cyprus contact the Shanda Consult Team now through the contact form below.

For more information on Cyprus Holding companies, please click here.

Disclaimer

Shanda Consult and the authors of this article explicitly disclaim any liability or responsibility to any individual, entity, or corporation that acts or fails to act based on any portion of this publication. Consequently, no individual, entity, or corporation should take action or rely on the information provided or implied in this publication without first seeking advice from a qualified professional or advisory firm, ensuring that the advice is tailored to their specific circumstances.

a