Cyprus International Trusts

The law governing the establishment of trusts in Cyprus is based on the English system. It is a combination of the English Principles of Equity and Statue Law. Cyprus International Trusts are regulated by the International Trusts Law 69(I)/1992 as amended by Law 20(I)/2012.

What is a Trust?

A trust is a settlement or legal agreement affecting at least three parties:

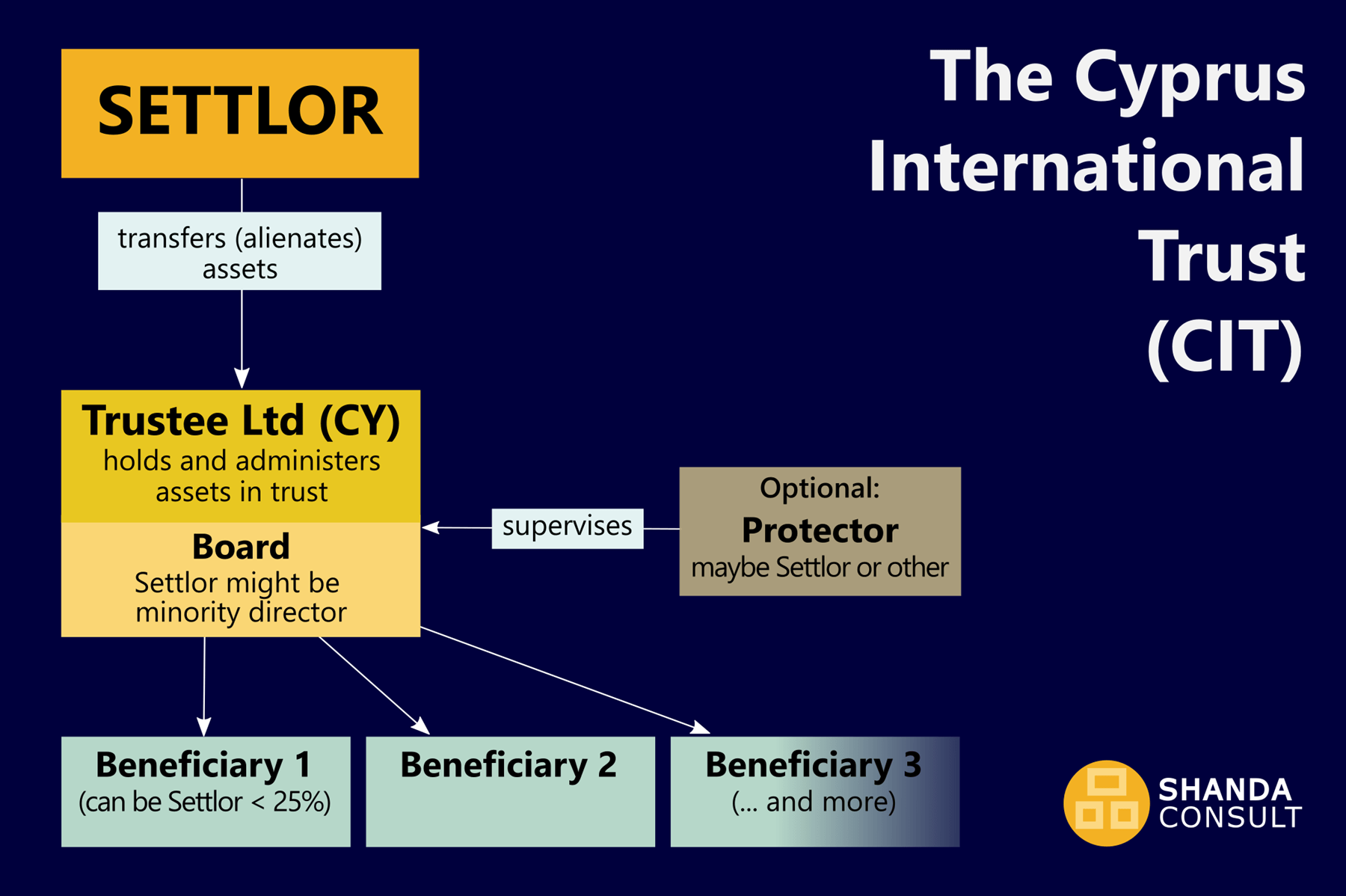

- The Settlor: (or Grantor, Trustor, Trust Maker); the person (natural or legal) who creates the trust; he/she is the owner of the property to be divested into a trust.

- The Trustee: legal or natural person, who agrees to hold the trust property in his/her/its name for the benefit of the Beneficiary, under the terms of the trust. Responsible for managing the property.

- The Beneficiary/Beneficiaries: individuals or companies or any other entities receiving the benefits of the trust property.

In a Discretionary Trust, instead of specifying specific persons or entities as beneficiaries, classes of beneficiaries are defined, for example “all current and future children of Mrs X”, or “charity organisations providing education for refugees and their children in the UK”. - The Protector: individuals or companies that are typically appointed by the settlor to protect the trust assets. The settlor of a Trust may act as protector as well.

Appointing a protector is optional. The protector has the right to control the trustee, but does not have the right to intervene in the trustees obligations and undertakings. The protector has the right to dismiss a trustee.

If a protector intervenes a trustee’s duties or has been granted the right to do so in the Trust Deed, a trust may be recognized as a “sham trust” or “illusionary trust” and thus being considered or even declared void.

Settlement of Trust – Trust Deed

A trust is a fiduciary relationship in which the settlor gives the right to the trustee to hold title to a property (trust property) for the benefit of the beneficiary. The trustee has the legal title to the trust property, whereas the beneficiary has the beneficial title to the trust property. The ultimate beneficial owners of the trust property is/are the beneficiaries.

Consequently, the trustee is the legal owner of a trust’s assets, but not the beneficial owner, which is the beneficiary or beneficiaries or classes of beneficiaries.

Trusts are established to provide legal protection for the settlor’s assets; for the purposes of wealth management, investment, social goals, charities, succession planning or sometimes tax planning.

The law imposes a strict duty of confidentiality on the trustee about the trust and the identity of the settlor and beneficiary. It is only possible to disclose such information in case of a court order in any civil or criminal proceedings when the court is convinced that such information is important to the outcome of the proceedings.

The main duties of a trustee is to administer the trust property prudently and to comply with the terms of the trust. The terms of a trust are set in the Settlement of Trust, also referred to as Trust Deed or Trust Instrument. Any action taken by a trustee that contravenes the terms of the trust deed is a ‘breach of trust’ and makes the trustee personally liable for the full extent of any loss incurred.

The Settlor has the right to reserve some powers, such as to revoke or amend the trust or to remove and appoint trustees.

All trusts related matters are determined in accordance with Cyprus Law.

Letter of Wishes for a Trust

In addition to the Trust Deed with its provisions and instructions how the assets of the trust shall be managed etc., a settlor may additionally opt to draft and hand over to the trustee a so-called Letter of Wishes.

A Letter of Wishes is not legally binding for the trustee but shall provide guidance to the trustee on how to manage the trust. A Letter of Wishes is not mandatory.

Unlike a Trust Deed, a Letter of Wishes remains discretely with the trustee. Neither courts nor beneficiaries have the right to demand disclosure of a Letter of Wishes.

Requirements to create a valid

Cyprus International Trust

- The following three certainties must be present:

Certainty of Intention: Evidence of express intention of the settlor to create the trust. This is evidenced by the Trust Deed.

Certainty of Subject Matter: The trust property must be readily identifiable otherwise the trust is void for uncertainty.

Certainty of Objects: The identity of all the beneficiaries of the trust must be ascertained or ascertainable at the time of setting up the trust.

- The Settlor shall be of sound mind and of right age.

- The Settlor (being either a natural or legal person) shall not be a resident of Cyprus for more than one year at the time when a CIT (Cyprus International Trust) is established.

- The beneficiaries shall not be residents of Cyprus at the time when a CIT (Cyprus International Trust) is established. They may become resident of Cyprus once a trust has been established.

- The trust property can include all kinds of assets situated in Cyprus or anywhere in the world.

- At least one of the trustees must be resident of Cyprus during the whole duration of the trust.

- It is advisable to incorporate a provate company limited by shares to act as trustee.

- The settlor may be appointed as minority director of the “Trustee Ltd”.

Cyprus Discretionary Trusts

There are various forms of trusts existing, based on certain details; for a list of trust types, please see the end of this article.

Cyprus discretionary trusts are trusts with now specific individual beneficiaries defined and the selection of beneficiaries as well as their benefit left to the discretion of the trustee.

In case of defining specific individuals or entities as beneficiaries, the settlor, in the trust deed, defines classes of beneficiaries. There is no limit to the definition of classes of beneficiaries, which could be, for example, “all current and future children of Mrs X”, or “charity organisations providing education for refugees and their children in the UK”, or “the elderly houses in my city”.

The settlor may define projects or areas in the Trust Deed, for which the assets, or if preferred so, the gains from the assets, shall be used. A brief example of definition of benefits and beneficiaries: “education costs and financing of viable startups of my children and grandchildren”.

It is then left to the trustee to decide when and how the trust will fulfill those provisions of the Trust Deed. If, after having finalised their education, only one of three children runs a viable startup, only that one child qualifies for benefiting from startup financing by the trust.

An advantage of a Cyprus Discretionary Trust is that none of the members of the class of possible beneficiaries has a right for claims against the trust.

The members of a class of beneficiaries become beneficiaries once the trustee decides as per the provisions of the Trust Deed, and perhaps of the Letter of Wishes.

As long as the members of the class of beneficiaries did not become actual beneficiaries, they cannot be held tax-liable for any assets and gains of assets of the trust, because they cannot be assumed as beneficiaries.

Trustees

It is important that a settlor chooses a person of trust as the trust’s trustee, typically being the director(s) of a limited company set up as trustee entity. Furthermore, a trustee should have asset management and business qualities and experience, because the trustee will be the person who will manage the assets of a trust, as per the provisions of the trust deed and a possible letter of wishes and under the supervision of a possible protector.

It is advisable to set up a company in Cyprus for the purpose of acting as the trust’s trustee entity. The directors of that company are managing the assets entrusted by the settlor. It is important not to appoint so-called “nominees” without management background, which might lead to the undesired result that a trust is recognized as a sham trust or illusionary trust, because it cannot be assumed that a trustee without the necessary management capabilities is able to manage the assets of a trust without a substantial involvement of the settlor.

The settlor might be appointed as a minority director, for example being one of a total of three directors. However, substantial involvement of a settlor would be contradictory to the idea and spirit of a trust, to which a settlor entrusts assets for the management by the trustee and for the benefit of the beneficiaries. In such cases, despite the settlement of a trust, that trust might be recognized by courts as not existing.

Cyprus Trust Registry

The law imposes the obligation on resident trustees to register Cyprus International Trusts with the Trusts Register (“Beneficial Ownership Register of Express Trusts and Similar Legal Arrangements”) kept by the Cyprus Securities and Exchange Commission (CySEC). The entry into the Trusts Register shall contain the following information about the Trusts:

- Name of the trust;

- Date of creation of the trust;

- Date of termination of the trust;

- Settlor(s): name and surname, date and place of birth, nationality, residential address, identification document and other relevant information;

- Trustee(s): name and surname, date and place of birth, nationality, residential address, identification document and other relevant information, or in case of a corporate trustee, name, type and registration number, etc. of the legal person;

- Beneficiary(ies) name and surname, date and place of birth, nationality, residential address, identification document and other relevant information;

- Protector: name and surname, date and place of birth, nationality, residential address, identification document and other relevant information;

- Date of any change in the law governing the trust to or from Cyprus Law.

The Registers of Trusts are not available to the public, but they are available for inspection by the Competent Authorities, such as:

- competent supervisory authorities, tax authorities, the customs department, the unit for combating money laundering (MOKAS), and the police;

- supervised/obliged entities within the context of conducting client due diligence and identification procedures;

- any person that, upon the submission of an application to CySEC, proves a legitimate interest; and

- any legal or natural person that submits an application to CySEC in relation to an express trust or a similar legal arrangement holding or having in its control, controlling interest in a company or other legal entity, either through a direct or indirect ownership status, or through bearer shares or through control with other means.

Benefits of Cyprus International Trusts

Asset protection

- A Cyprus International Trust may be used to protect assets against risks, future claims by governments or creditors, expropriation etc.

- Future protection from creditors.

- Future protection from claims of spouses or former spouses.

- A Cyprus International Trust can be utilized to protect assets against future claims in tort or contact because of transactions entered by the previous owner of the trust property.

Confidentiality and reporting

- The trustees owe duty of confidentiality to the settlor and to the beneficiaries. They are not allowed to disclose any information or documents unless they are ordered to do so by a specific court order.

- However; registration of the Cyprus International Trust in the Trusts Registry is mandatory, please see details above.

- No reporting requirements for Cyprus International Trusts in Cyprus.

- Please note that in the case of bank account opening on behalf of a trust, the settlor, the trustee, the protector (if any) and the beneficiaries (if they are not defined as a class of beneficiary without naming them) are legally subject to full due diligence and compliance procedures.

Managing family wealth, estate planning, inheritance planning

- A Cyprus International Trust is ideal for asset planning of high net-worth individuals with extended or complicated family structures.

Tax benefits

- Income, gains and profits from non-Cyprus sources are exempt from taxes in Cyprus.

- The worldwide income, gains and profits are taxable in Cyprus only if the beneficiary is tax resident in Cyprus.

- Beneficiaries who are non-tax residents of Cyprus are taxed only on Cyprus sourced income in accordance the Income tax law of Cyprus.

- Dividends, interests or royalties received by a Cyprus International Trust from a Cyprus company are not taxable and not subject to any withholding tax.

- No estate duty/inheritance tax.

Reservation of Powers

- When setting up the trust the settlor may reserve powers to him/herself specifically drafted into the trust instrument. Such powers are: to revoke, vary or amend the terms of a trust; to appoint or remove any trustee/enforcer/protector/beneficiary/investment adviser; to give (very limited) directions to the trustee etc.

Perpetuity period

- Trusts may exist for the duration of a lifetime plus 21 years or in the case where no natural person is involved it can exists for merely 21 years.

No exchange control regulations

Types of Cyprus International Trusts

- Private Trusts

- Express Private Trusts

- Resulting Trusts

- Constructive Trusts

- Implied Trusts

- Charitable Trusts

- Fixed Trusts

- Discretionary Trusts